Faculty Research

Decoding Market Uncertainty through Information Measures

Financial markets are often seen as unpredictable, with prices constantly moving due to news, investor behavior, and global events. While many approaches focus on predicting these movements, an equally important question is: how uncertain is the market itself?

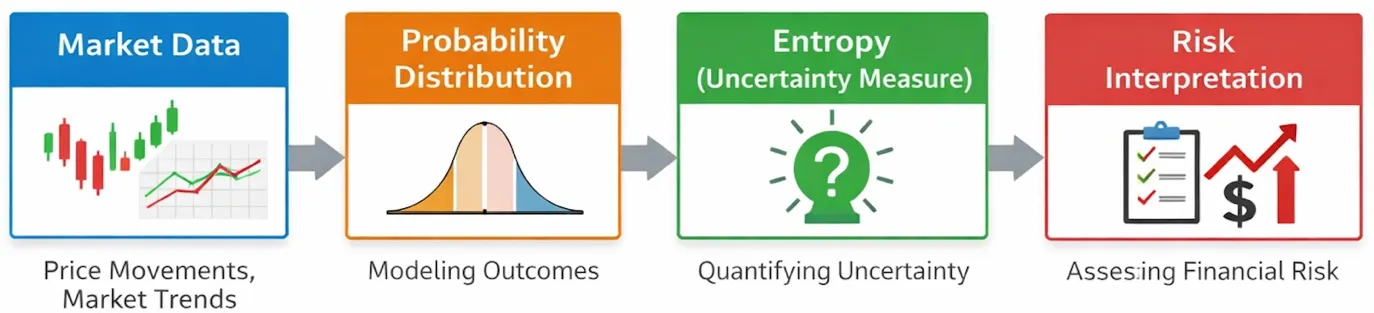

This research addresses this question using concepts from information theory, which helps us measure uncertainty in a systematic way. Instead of simply forecasting prices, it examines how much randomness or unpredictability is present in market behavior using measures such as entropy.

To put it simply, this approach tries to measure how “surprising” market movements are. A highly unpredictable market carries more uncertainty, while a more stable one is easier to understand and anticipate.

By quantifying uncertainty, this research provides deeper insights into financial risk and helps improve decision-making for investors, analysts, and policymakers. It shifts the focus from just predicting outcomes to understanding the reliability of those predictions.

How uncertainty is measured in this research:

Measuring uncertainty in financial markets is similar to weather forecasting.

Instead of saying “it will rain,” it is more useful to say “there is a 70% chance of rain.”

This research brings a similar perspective to finance.